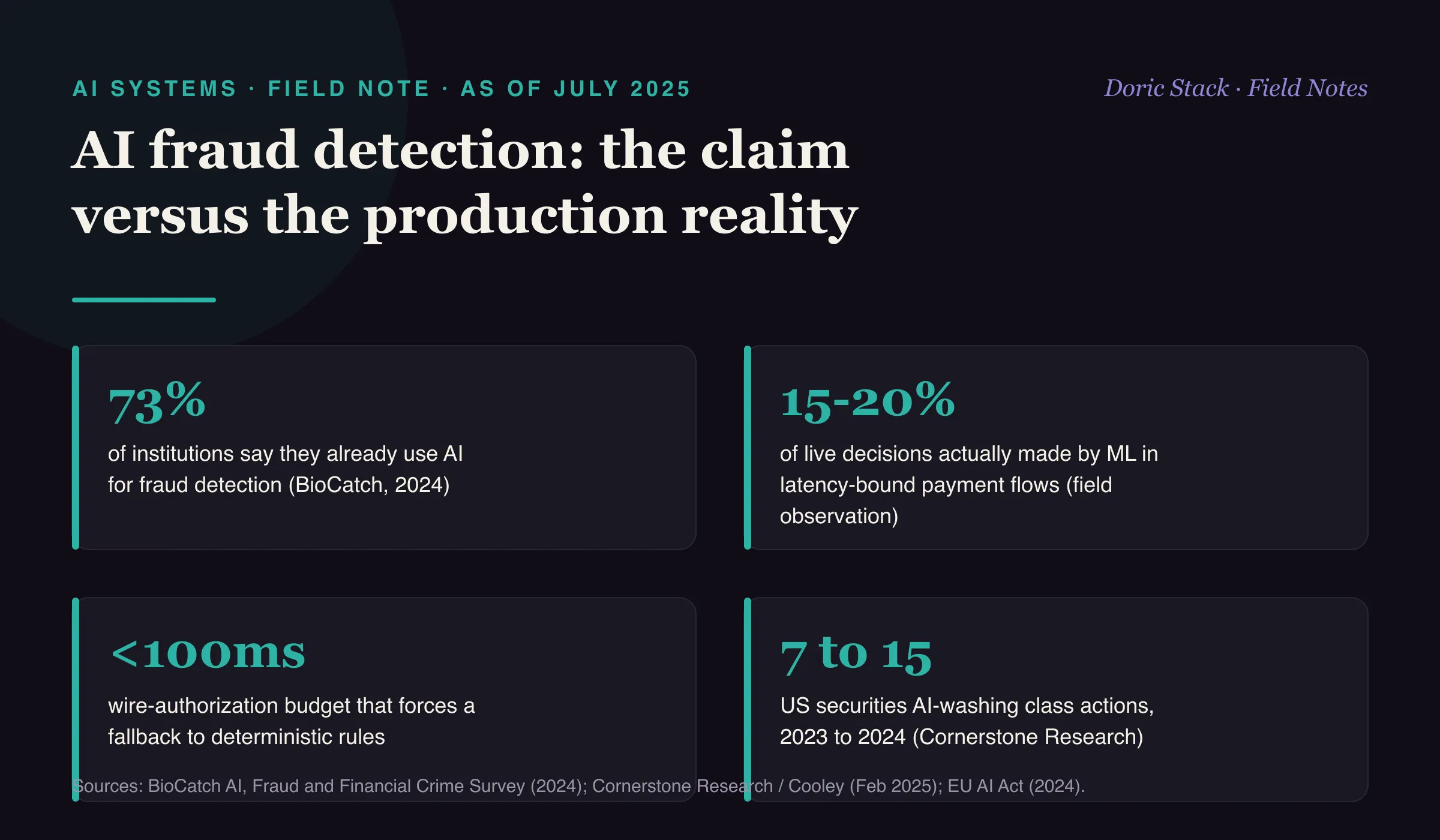

As of July 2025

Marketing decks show a deep-learning model and a glossy dashboard. Production tells a quieter story: when money has to move at the speed of a blink, that model is not in the critical path.

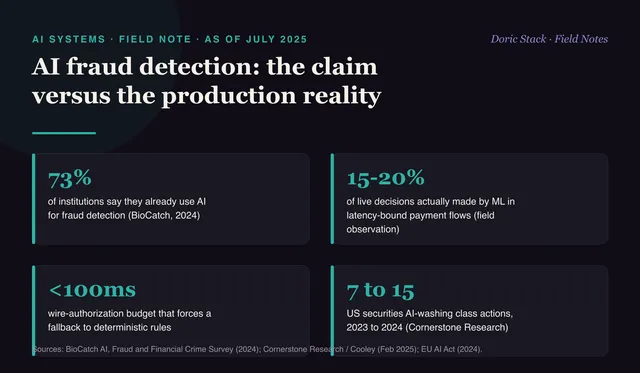

Calling a system “AI-powered” without saying where the rules still win is the gap regulators and investors have started to punish. Nearly three-quarters of banks claim AI fraud detection; far fewer can show what the model actually decides once a transaction hits the latency budget.

Adoption claim

73%

of institutions say they already use AI for fraud detection (BioCatch, 2024).

Latency budget

<100ms

the wire-authorization window; heavyweight inference does not fit, so the engine falls back to deterministic rules.

AI-washing suits

7 to 15

US securities AI-washing class actions, 2023 to 2024 (Cornerstone Research, via Cooley, Feb 2025).

The disconnect shows up the same way in implementation after implementation. A bank buys an ML fraud platform, demos it on deep-learning inference, then quietly routes live authorization through threshold rules because the model cannot answer inside the budget. In my experience the model ends up making something like 15 to 20 percent of the real decisions, and rule logic carries the rest. That is not a failure, it is physics. It becomes a problem only when the marketing claims otherwise.

What actually works

Hybrid decision engines: lightweight ML flags anomalies, and deterministic logic or a human resolves the edge cases. Simple ensembles earn their place - gradient-boosted trees often outscore giant neural nets once you weigh latency, explainability, and drift monitoring together. The win is not the biggest model; it is the model that survives production constraints and still answers in time.

Where the claims break

Drift is the honest tell. Across the fraud platforms I have seen, material model drift appears within six to twelve months, well before the annual “model refresh” most governance decks assume. If you cannot measure drift, you cannot defend the AI claim.

The banks that win with AI are not the ones boasting about quantum-scale models. They are the ones honest about where rules still beat ML.