As of January 2026

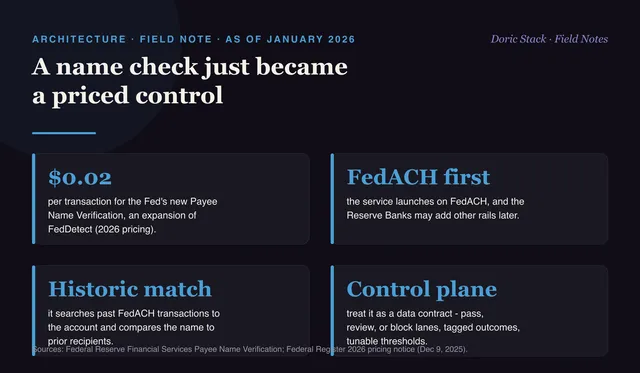

A name check just became a priced control in US payments. The Fed's 2026 pricing notice introduces Payee Name Verification, an expansion of FedDetect Notification Services, at two cents a transaction, starting on FedACH.

That changes the architecture, not just the UI. From an architect’s view this is not a yes-or-no check bolted on at the edge. It is a new control point that reshapes routing, exception handling, and reconciliation.

How it works is what makes it architectural. The service searches historic FedACH data for past transactions to the payee account and compares the submitted name against the names previously associated with it. So the answer is not a clean yes or no. It is a match, a near-match, or nothing on file, and each of those is a different downstream decision. A control that returns three shapes of answer needs three lanes built for it.

Price

$0.02

per transaction for Payee Name Verification, an expansion of FedDetect Notification Services (2026 pricing).

First rail

FedACH

the service launches for FedACH customers, and the Reserve Banks may add other rails later.

Mechanism

Historic match

it searches past FedACH transactions to the account and compares the submitted name to prior recipients.

Not a yes-or-no check

It is a control point. Where it sits in the flow, what each result triggers, and how the outcome is recorded all become architecture decisions the moment you turn it on.

Design it as a data contract

Normalize and tokenize the name data before submission so formatting differences do not manufacture false mismatches. Set match policy by use case, because payroll, treasury, bill-pay, and A2A transfers should not share one threshold or one action. Build a three-lane decision model - pass, review, or block - each with its own SLA and customer messaging. Tag the payment record with the check outcome so disputes, audits, and returns trace without reconstructing history. And add feedback loops so operations tune thresholds against real exception rates rather than assumptions.