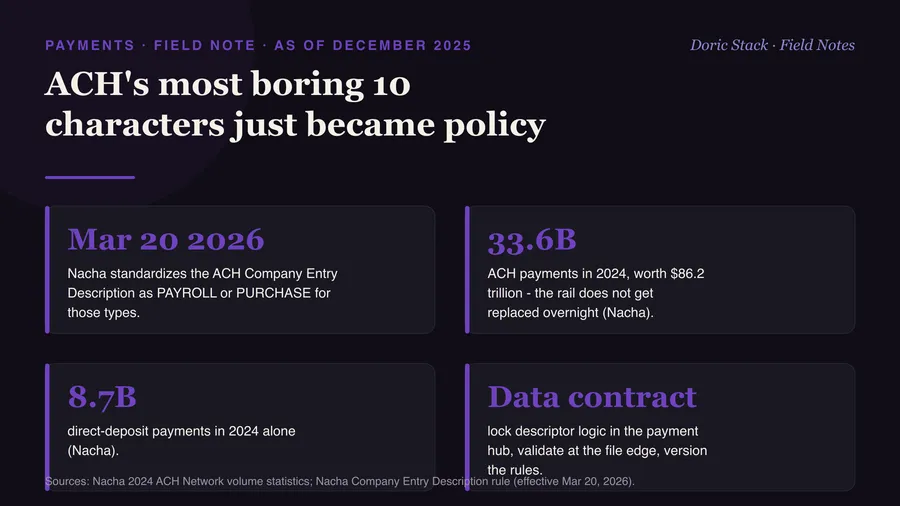

As of October 2025

Pay-by-bank looks like free money on the CFO's slide: process $50 million a month at 2.5 percent card fees and you are paying $1.25 million a year, so move to FedNow at about four and a half cents a transaction and most of that goes away.

The savings are real. The bill underneath them is the part nobody puts on the slide, and it lands on treasury, not finance.

The trap is operational, not technical. Treasury reconciles in predictable windows - 2 AM, 11 AM, 5 PM. Account-to-account payments do not respect windows. They arrive Saturday at 7:13 PM and Tuesday at 3:27 AM, continuously, and a batch process built for three runs a day was never designed for that. Continuous reconciliation means more staff, exception coverage around the clock, and middleware to keep running.

Per-transfer fee

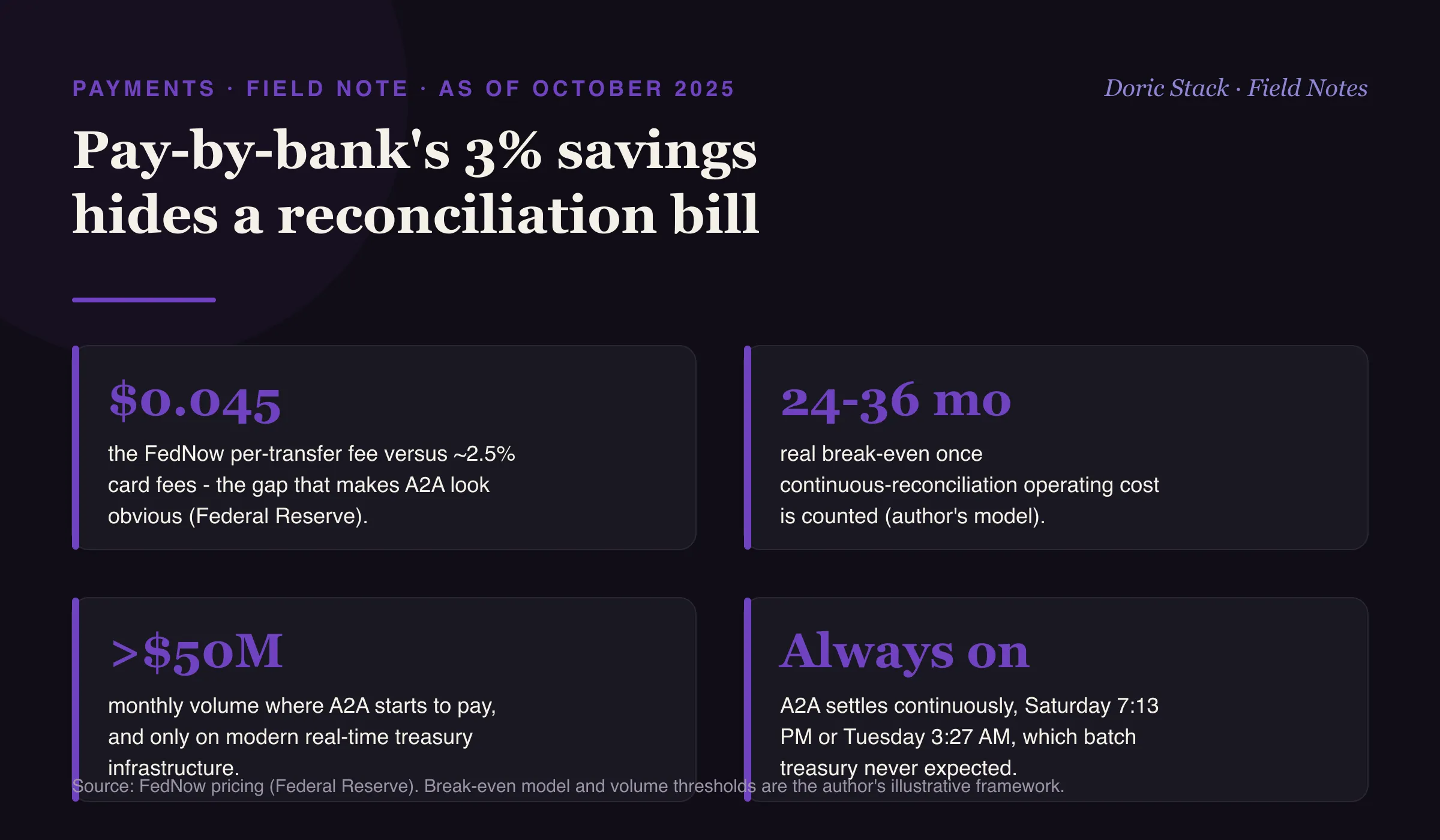

$0.045

the FedNow per-transfer fee against ~2.5 percent card fees (Federal Reserve pricing).

Real break-even

24-36 mo

once continuous-reconciliation operating cost is counted, not just the fee savings (author model).

Volume floor

>$50M

monthly volume where A2A starts to make sense, and only on modern real-time infrastructure.

The headline number

Card fees at 2.5 percent on $50 million a month is $1.25 million a year. FedNow at about four and a half cents a transaction erases most of it. That is the slide.

The number under it

Implementation runs $1.2 to $1.8 million upfront, then continuous operations add real cost. In this worked example, two more treasury staff, around-the-clock exception handling, and middleware maintenance turn a $1.2 million gross saving into roughly $600,000 net, and break-even moves from “obvious” to 24 to 36 months. Below $30 million a month, the return takes longer than three years. The numbers are an illustration, but the shape holds: the savings are in the fee, the cost is in the reconciliation.