As of August 2025

When a payment fails, the reversal is the cheap part. The expense is everything after: the research, the compliance review, the correspondent-bank back-and-forth, the escalation to save the relationship.

Banks meter fraud to the dollar and leave exception handling as an unmeasured cost center. It is one of the largest operating costs in payments that almost nobody puts a number on.

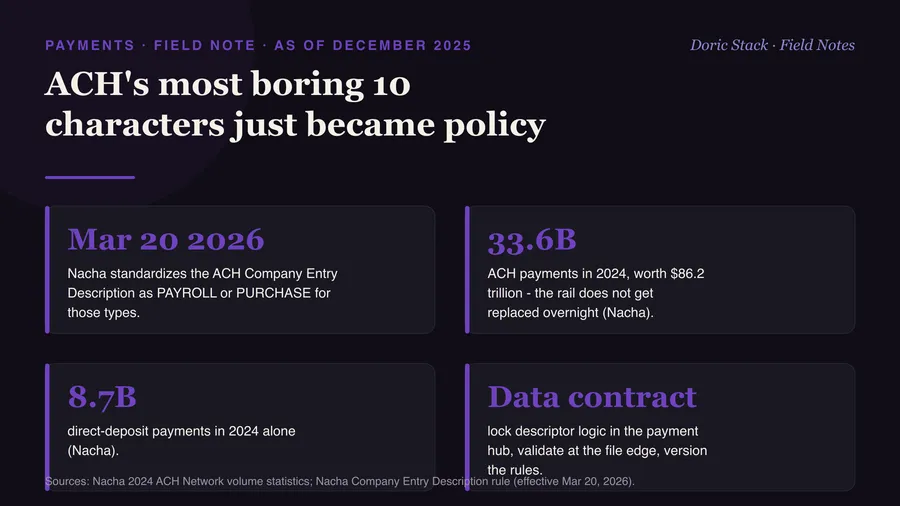

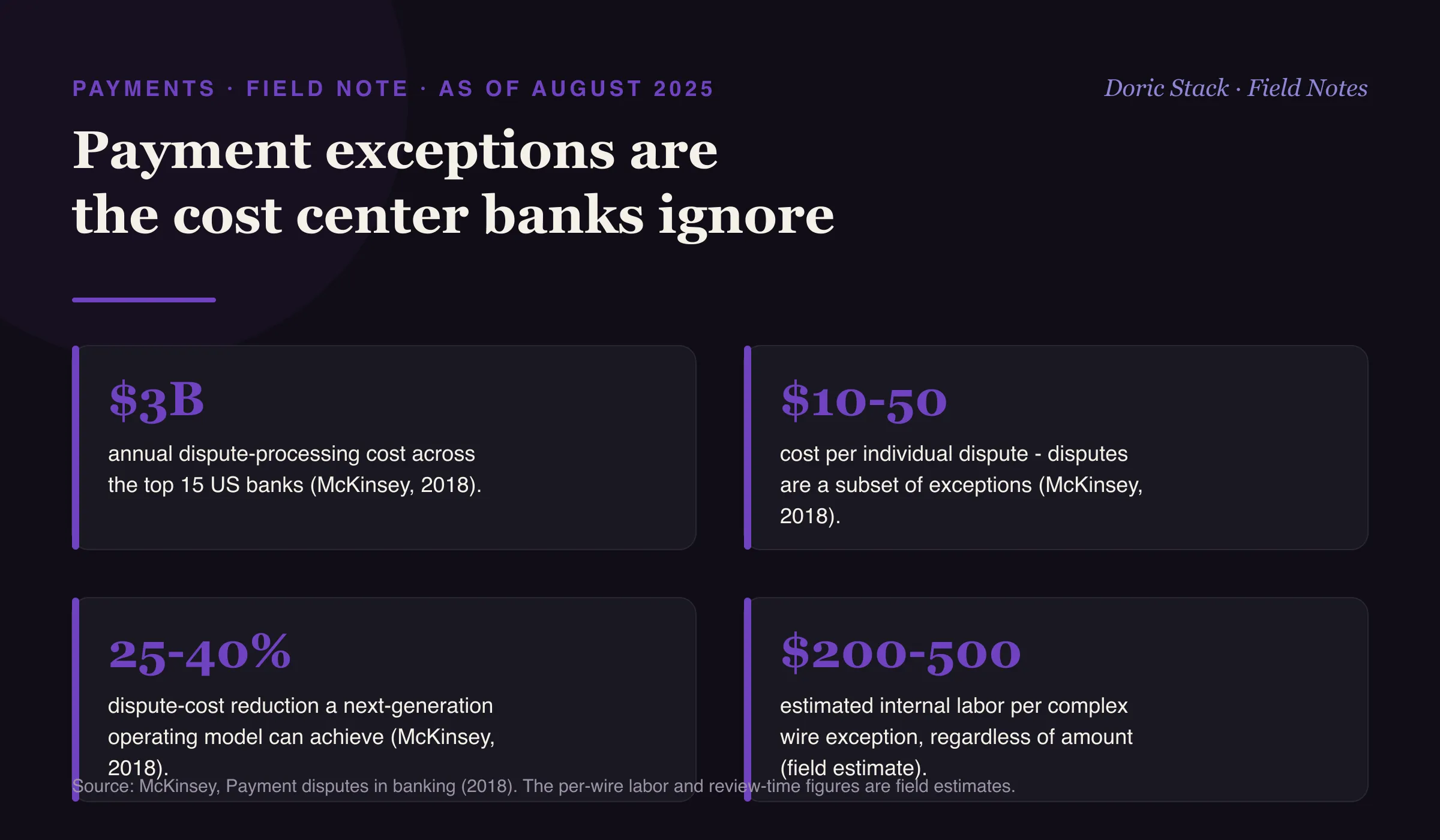

Start with the one figure that is well sourced. McKinsey put dispute processing across the top 15 US banks at roughly $3 billion a year, at $10 to $50 per dispute. Disputes are only a slice of exceptions - ACH returns, wire recalls, and RTP or FedNow errors that often have no clean resolution path all land on the same operations teams - so the true exception bill sits above that line, not below it.

Dispute spend

$3B

annual dispute-processing cost across the top 15 US banks (McKinsey, 2018).

Per dispute

$10-50

cost per individual dispute, a subset of all payment exceptions (McKinsey, 2018).

Reducible

25-40%

of dispute cost a next-generation operating model can remove (McKinsey, 2018).

The cascade

A flagged $50K wire does not resolve itself. Customer service fields the call, compliance runs a manual review, the correspondent bank gets looped in, legal weighs a recall, and management steps in to protect the relationship.

The fix is operational, not heroic

The banks that win here are not preventing every exception. They resolve them faster with less manual work: automated categorization and routing, straight-through processing for common return codes, real-time customer notifications, and investigation templates with the compliance steps built in. McKinsey’s own figure is that a next-generation operating model can take 25 to 40 percent out of dispute cost. A single complex wire exception can still run an estimated $200 to $500 in internal labor regardless of the amount, which is exactly why automating the routine ones pays.