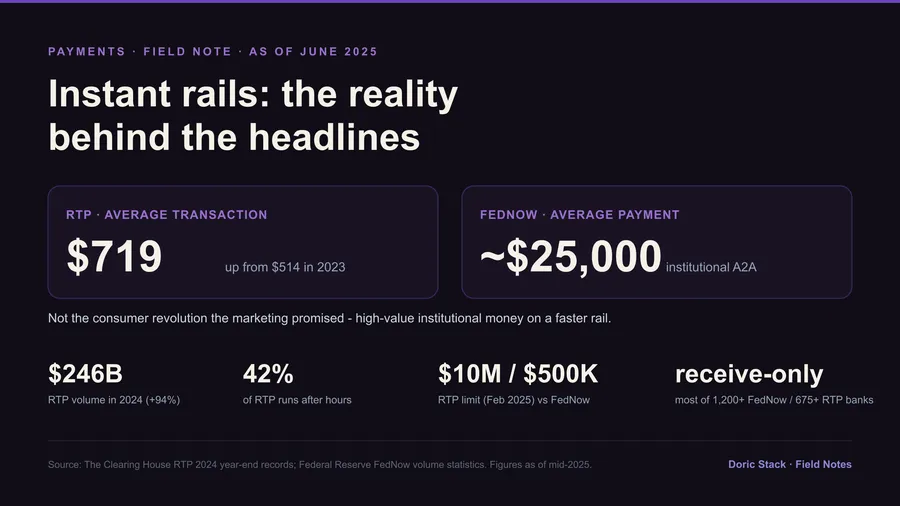

As of June 2025

A 20x transaction-limit gap between TCH-RTP and FedNow is quietly sorting banks - and their corporate customers - into a two-tier instant-payments system decided by transaction size.

An $8M commercial real estate deal got chopped into 16 separate payments this week because the buyer’s bank used FedNow, capped at $500K, while the seller expected one clean wire. A five-minute transaction became a three-hour coordination problem. That story is the whole strategic picture in miniature.

TCH-RTP limit

$10M

The Clearing House raised the TCH-RTP transaction limit to $10 million - built for high-value B2B and corporate disbursements.

FedNow limit

$500K

FedNow stayed at $500,000. A 20x gap that turns rail choice into a constraint on what a payment can even be.

The squeeze

Two-tier by size

Corporate treasurers now find their payment options depend on their bank technology choices, not their business requirements.

The instant-rails conversation usually gets framed as a technology race. It is not. Both rails clear in seconds. The thing actually separating them is a policy number: The Clearing House raised the TCH-RTP transaction limit to $10 million, and FedNow stayed at $500,000. That single gap is reshaping which institutions pick which rail, and which customers they can serve well.

The question is not which technology wins. It is whether this fragmentation serves customers, or just creates vendor lock-in by transaction size.

The divide, in one view

The original infographic for this note lays out the split: limits, ecosystem maturity, and the market-impact metrics behind the positioning.

The $10M strategic divide

Side-by-side rail positioning - limits, maturity, and the Q2-2024 market metrics - so the strategic split is visible at a glance rather than argued in prose.

The $10M strategic divide

Why the gap creates a two-tier system

Large commercial banks are gravitating toward TCH-RTP because corporate clients need the high-value capability. When a manufacturer wants to pay $2M for equipment, splitting it into four payments is not professional. Per recent industry data from U.S. Bank, TCH-RTP now handles over 1 million daily transactions, with 42% happening outside business hours - the shape of real corporate and consumer demand, not a pilot.

Community banks, meanwhile, appreciate FedNow’s federal backing and simpler onboarding. But they are discovering their business customers are larger than expected, which puts those customers on the wrong side of the $500K line. The corporate treasurer ends up caught in the middle: their available rail now depends on their bank’s technology choice, not on what their business actually needs to move.

A Payments Dive analysis frames where this leads: a two-tier system where transaction size determines which rail you can use. That feels backward. The rails were supposed to expand what payments could do, not quietly decide them by which institution you happen to bank with.