As of April 2026

Two US regulatory threads I have tracked for months just lined up. One builds the issuance layer for stablecoins. One builds the custody layer. Most people are filing them as separate news items. They are the same story.

In institutional digital-asset work, the blocking question is never the technology. It is regulatory standing: who holds the asset, under which legal framework, with what fiduciary obligations. The 48-state money-transmitter patchwork never answered that cleanly for institutions that need consistent standards.

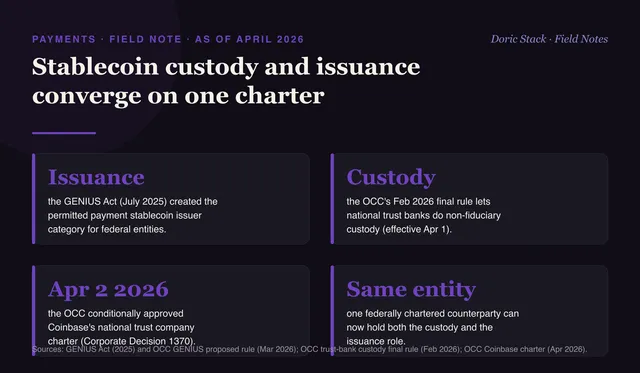

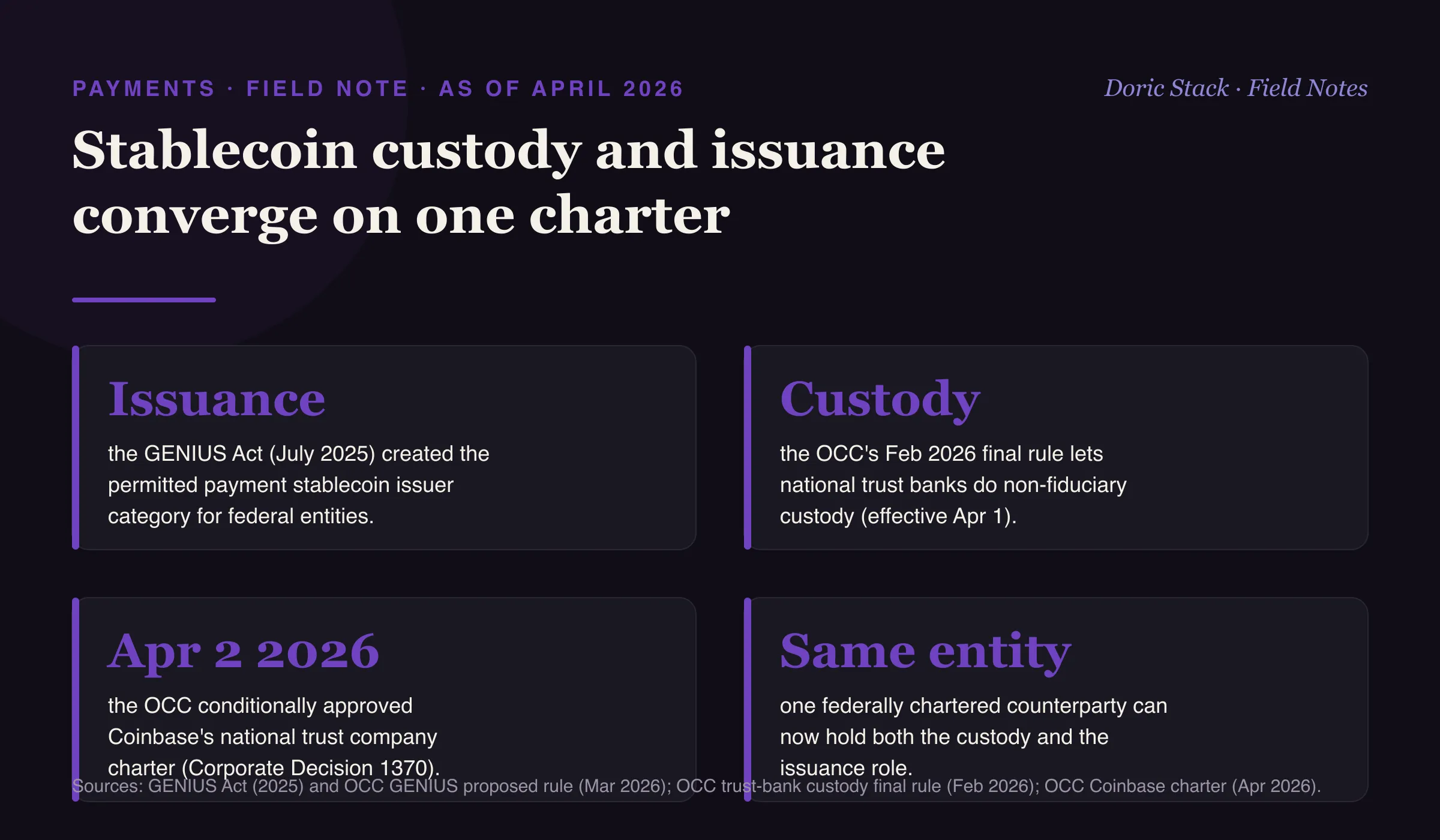

The two layers come from two distinct actions. On issuance, the GENIUS Act - signed in July 2025 - created the permitted payment stablecoin issuer category, and the OCC published its own proposed rule for OCC-supervised issuers in March 2026. On custody, the OCC’s February 2026 final rule confirmed that national trust banks can engage in non-fiduciary custody, taking effect April 1, 2026. The day after that rule went live, on April 2, the OCC conditionally approved Coinbase’s national trust company charter. The same kind of federally chartered entity can now sit on both sides.

Issuance layer

GENIUS Act

the July 2025 law created the permitted payment stablecoin issuer category for federally chartered entities.

Custody layer

OCC rule

the OCC's February 2026 final rule lets national trust banks do non-fiduciary custody (effective April 1).

The charter

Apr 2 2026

the OCC conditionally approved Coinbase's national trust company charter (Corporate Decision 1370).

Why the convergence matters

Settlement finality becomes a question you can actually answer: which entity holds the asset, under which legal standard, with which bankruptcy protections. That is the input institutional treasury teams have wanted before they commit capital.

How to design for it

When you build institutional digital-asset workflows now, model both layers explicitly. The custodian. The issuer. And the legal boundary between them. The new development is that those two roles can sit inside one federally regulated counterparty rather than being split across a trust company and a separate issuer under different frameworks. The rulemakings are still in motion, so treat the finality and insolvency questions as becoming tractable, not fully settled. But the direction is set: where regulated custody and regulated issuance converge, institutional capital tends to follow.