As of June 2026

At 3:17 AM, the confirmation never arrived. Two million dollars in institutional stablecoin. The custody record showed the transfer complete, the counterparty's treasury system showed it pending, and the smart contract state said something different from both.

That scenario does not have a clean resolution path yet, and that is exactly the gap institutions are walking into as they build digital-asset payment workflows. The architecture question finally has an answer. The operations question does not.

Architecture

Answered

the OCC custody standard is codified and the GENIUS Act issuance rules are being written.

Operations

Unanswered

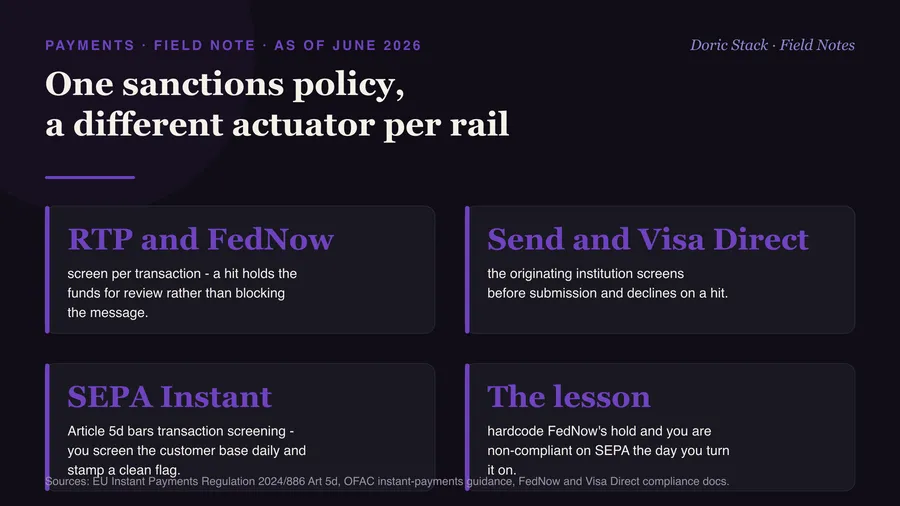

ACH has R-codes and wires have SWIFT gpi and FedLine investigations - stablecoin exceptions have none yet.

The move

Write runbooks

the institutions positioning well design exception playbooks before they go live, not after the first failure.

The regulatory stack is finally coherent

The architecture question has an answer now. The OCC custody standard is codified and took effect in April 2026. The GENIUS Act is law, and the issuance framework underneath it is being written, with the implementing rules in their comment stage. A bank can read the rules and know what compliant custody and issuance look like. That part is no longer the hard part.

The operations stack is not

Traditional payment exceptions have mature playbooks. ACH returns have R-codes. Wire investigations run through SWIFT gpi tracking and the Fedwire investigation request. There are escalation paths, correspondent relationships, and legal instruments for a disputed transfer, built over decades. Stablecoin payment exceptions have none of that yet.

Where the gap actually shows up

The hole opens in three specific places. First, who asserts settlement finality, and under which legal standard, when the chain and the books disagree. Second, where the asset sits when a smart contract is mid-execution and both legs read incomplete. Third, what the operations team calls when there is no equivalent of a SWIFT tracker to pull a transaction status from. None of those have a standard answer yet, which means each institution is writing its own or discovering it during an incident.

The institutions positioning well are not waiting for industry standards. They are designing exception playbooks before going live, writing runbooks for failure modes nobody has standardized yet.