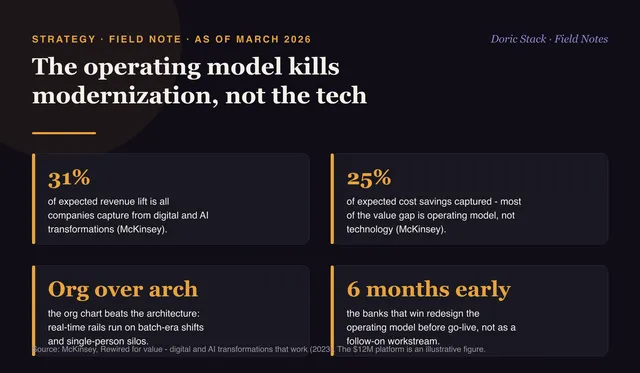

As of March 2026

The bank spent millions on a new payment platform and kept the same team structure, the same escalation matrix, the same three-person on-call rotation from 2019. The platform was modern. The operating model was legacy.

Most payment modernization failures are not technology failures. They are operating-model failures, and the gap shows up the first time real-time money meets a batch-era process.

Revenue lift captured

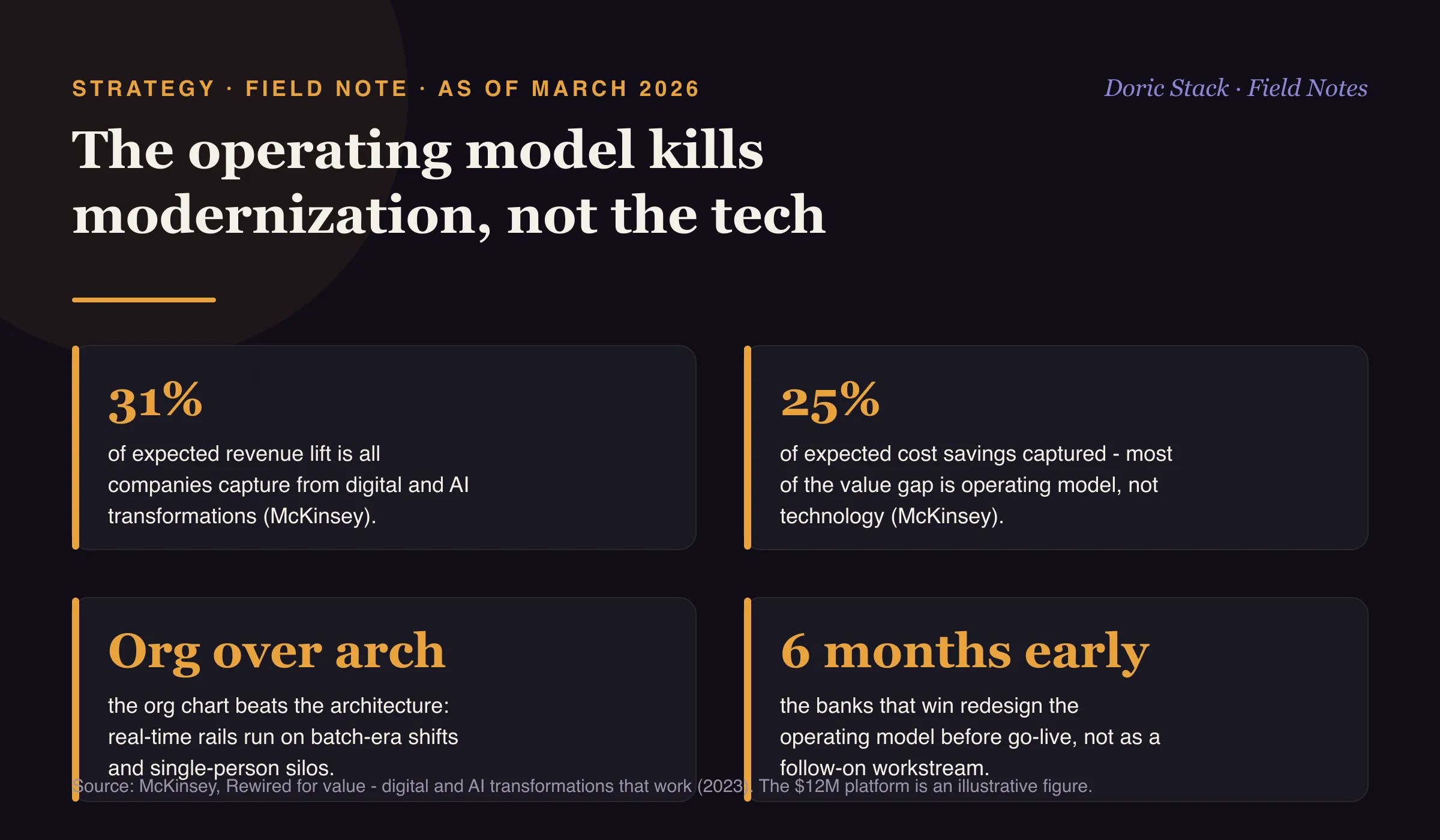

31%

the share of expected revenue lift companies actually capture from digital and AI transformations (McKinsey).

Cost savings captured

25%

of expected cost savings - most of the value gap lives in the operating model, not the technology.

Start early

6 months

the banks that win redesign the operating model before go-live, not as a follow-on workstream.

Where the mismatch shows

You deploy real-time rails but run operations in batch-era shifts, so FedNow settles in seconds while exceptions queue until Monday because nobody staffed the weekend. You build multi-rail routing but keep knowledge in single-person silos, and “only Dave knows wires” holds right up until Dave takes leave during a Fed deadline. You ship micro-services on continuous deployment, then gate every change behind quarterly cycles and six-week freezes.

What the winners do differently

They treat operating-model redesign as a prerequisite, not a follow-on workstream. They start roughly six months before go-live. They rebuild teams around rail-specific pods instead of one monolithic support queue, and they design escalation paths that match settlement speed rather than batch-era SLAs. The platform changing is the easy half. The operating model changing is the half that actually decides the outcome.

The hardest conversation in payment modernization is not technology selection. It is telling a room of people who have run operations well for a decade that their operating model has to change as much as the platform does.