As of December 2025

Euro payments now name-check you before they move. Since October 2025, a euro credit transfer runs a Verification of Payee check against the payee's name and IBAN, and a mismatch returns an alert before the money goes.

This is a euro-area obligation on the banks, but the operational hit travels. A US treasury paying EUR vendors, payroll, or marketplaces feels it the moment a supplier name in the ERP does not match what the receiving bank holds.

What actually went live

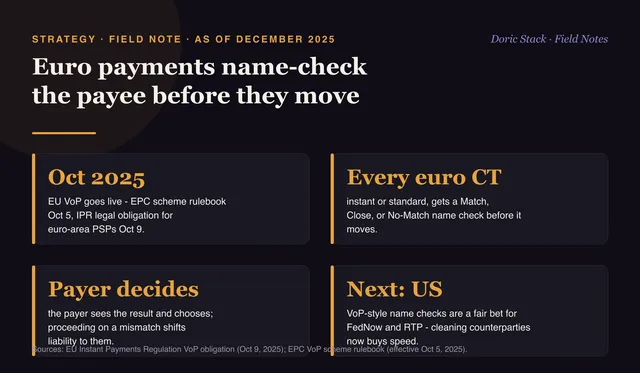

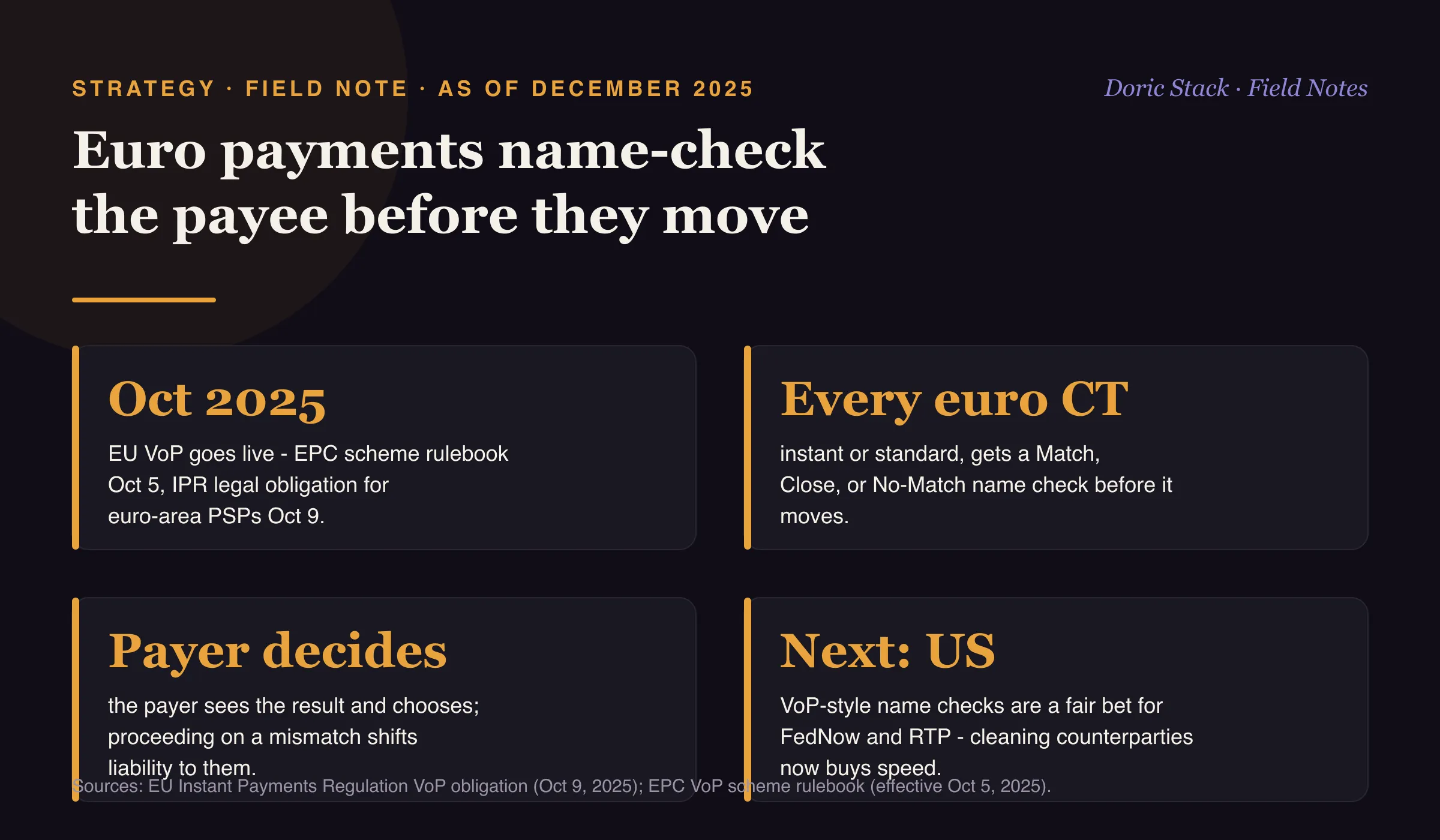

Two dates, often blurred into one. The European Payments Council’s VoP scheme rulebook took effect on October 5, 2025, setting the bank-to-bank messaging standard. Four days later, on October 9, the EU Instant Payments Regulation made offering VoP mandatory for payment service providers in the euro area. The check runs on every euro credit transfer, instant or standard, and returns a Match, Close Match, No Match, or “not possible” result that the payer sees before deciding to proceed.

Why a US treasury feels it

The obligation sits with the euro-area bank, not the foreign payer, but the failure shows up in your run. A EUR payment lands at a euro correspondent, becomes a SEPA credit transfer, and the VoP check fires there. If your supplier master does not mirror the bank’s record, the payment slows or stalls, and authorized-push-payment fraud only falls when someone actually actions the alerts rather than waving them through.

Now live

Oct 2025

EPC VoP scheme rulebook took effect Oct 5, and the IPR made it mandatory for euro-area PSPs from Oct 9.

Scope

Every euro CT

instant or standard, gets a Match, Close Match, or No Match name check before it moves.

Who decides

The payer

sees the result and chooses - proceeding on a mismatch shifts liability to the payer.

If your controls move slower than the payment, the rail will decide for you. Clean the counterparty data and build the alert lane before the same check lands at home.