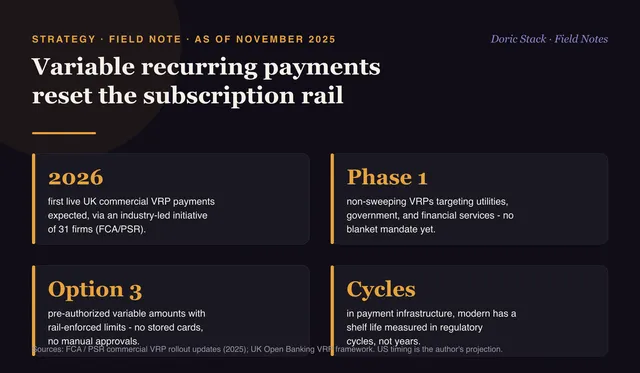

As of November 2025

Variable recurring payments solve the problem subscription billing has always had. Netflix charges the same amount monthly, but utilities, cloud bills, and usage-based services change every cycle.

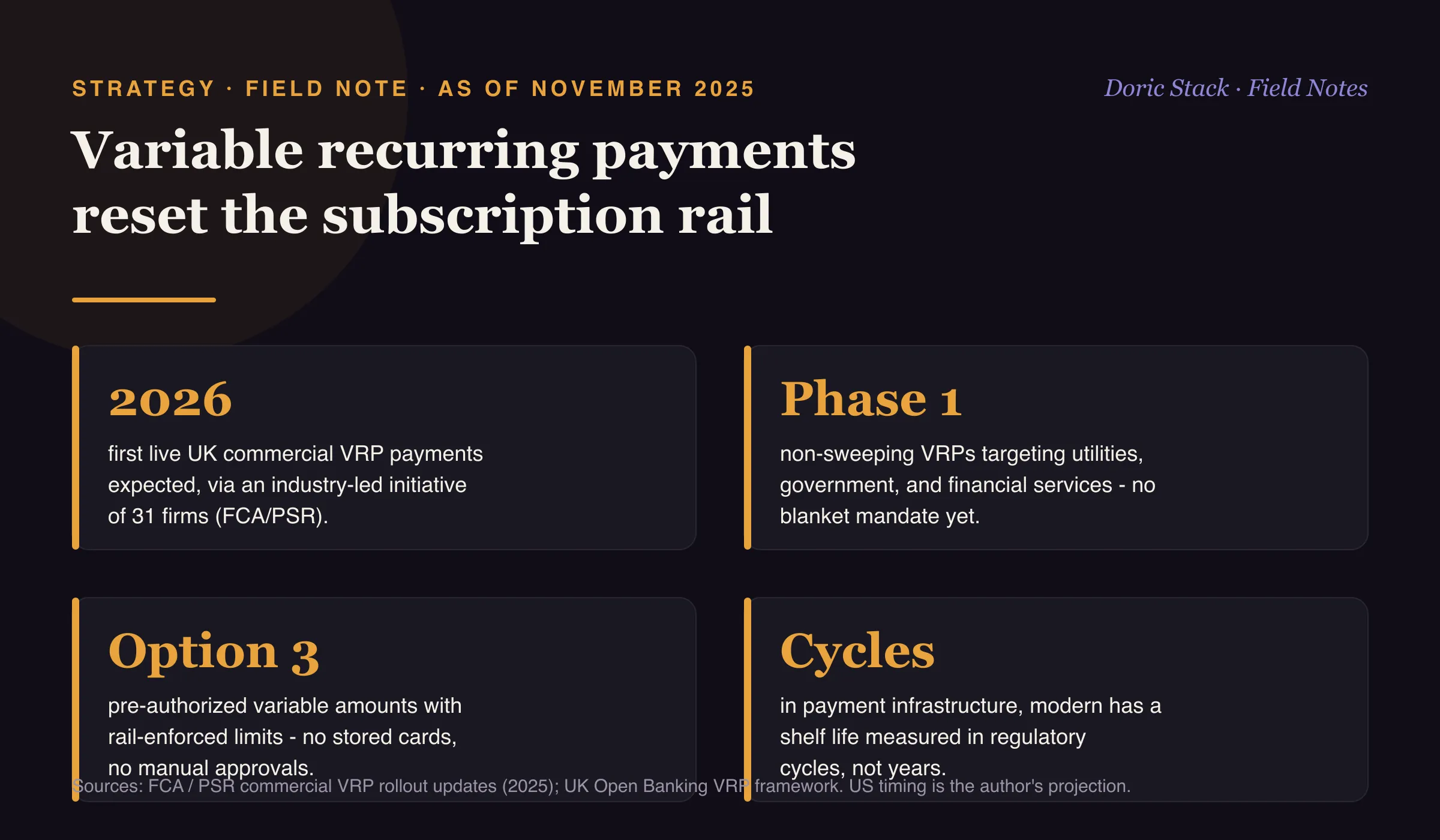

The only ways to handle variable billing today are storing a card, which is a compliance burden, or asking for manual approval every time, which is an abandonment problem. VRPs add a third option: a customer authorizes “charge me up to $500 a month,” and the payment rail enforces the limit.

How a VRP works

The consent lives at the rail, not the merchant. The customer sets the cap, the frequency, and the amount ceiling at authorization, and the bank enforces them on every charge. No stored card, no manual approval each cycle, and no 3 AM fraud alert because a model flagged a legitimate $487 bill as unusual. It is pre-authorized and bounded, which is exactly what variable billing needs.

Where the UK actually is

Despite the headlines, this is a phased, industry-led rollout, not a blanket mandate. A new industry body backed by 31 firms was being stood up through 2025 under the FCA and PSR, with Phase 1 aimed at utilities, government, and financial services, and first live commercial payments expected in 2026. The direction is set. The calendar is slower than the slideware suggests.

The third option

Pre-authorized

variable amounts with rail-enforced limits - no stored cards, no manual approval each cycle.

UK scope

Phase 1

non-sweeping VRPs target utilities, government, and financial services (FCA and PSR).

First live payments

2026

expected for UK commercial VRPs, via an industry initiative of 31 firms.

In payment infrastructure, 'modern' has a shelf life measured in regulatory cycles, not years. The instant-rails platform finished in 2022 is already a step behind.